What is a good credit score?

A good credit score is generally somewhere between 661 and 780. But what’s considered a good credit score depends on where a score comes from, who calculates it and who judges it. Lenders may set their own credit policies and standards to determine creditworthiness. And the way scores are calculated varies between scoring companies. For example, FICO® considers anything between 670 and 739 a good credit score, while VantageScore® says good credit scores fall between 661 and 780.

Keep reading to take a closer look at credit scores, including how they’re determined, who’s looking at them, and what you can do to monitor and improve yours.

What you’ll learn:

-

Most people have multiple credit scores, which vary based on how they’re calculated, when they’re calculated and what information is used to calculate them.

-

FICO and VantageScore are two popular credit-scoring companies.

-

Scores from FICO and VantageScore typically range from 300 to 850.

-

FICO says good credit scores fall between 670 and 739.

-

VantageScore says good scores fall between 661 and 780.

Why are there different credit scores?

Credit-scoring companies use different models to calculate credit scores. So, what FICO and VantageScore consider to be good scores can vary. And models might weigh information in credit reports differently as part of their calculations. That’s why your scores may vary, even if just by a few points, when you compare them.

According to the Consumer Financial Protection Bureau (CFPB), credit scores are based on information from your credit reports. FICO and VantageScore credit scores generally range from 300 to 850. Lenders, like credit card issuers or banks, ultimately determine for themselves what they consider a good credit score.

This video explains a little more about how credit works:

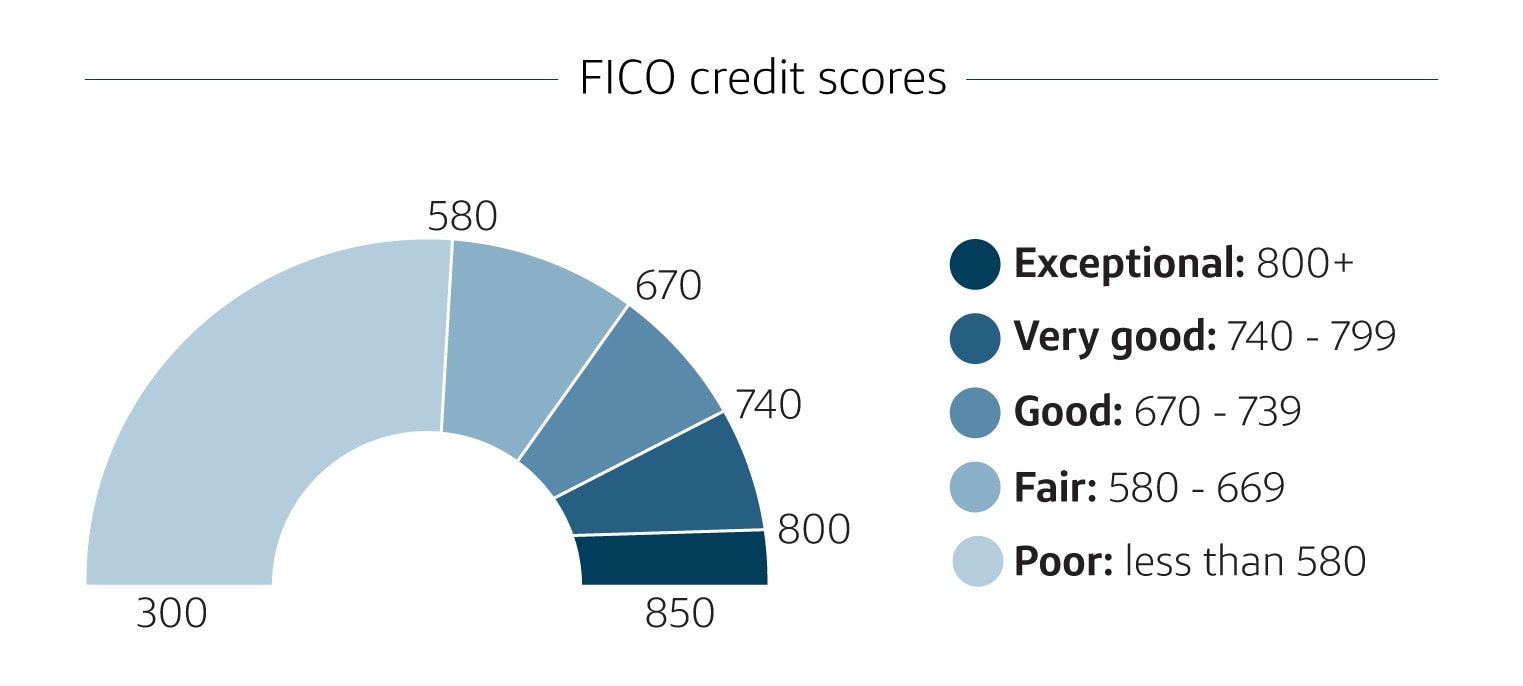

What is a good FICO score?

A good FICO score falls between 670 and 739. Scores in that range are near or slightly above the U.S. average credit score. FICO’s highest credit score is 850, and it breaks its scores into the following five categories:

Source: MyFICO.com

-

Exceptional: 800-850

-

Very good: 740-799

-

Good: 670-739

-

Fair: 580-669

-

Poor: less than 580

FICO also has consumer credit scores tailored to different industries, such as auto and mortgage lending. These industry-specific scores range from 250 to 900, but the same range of 670 to 739 is still considered good.

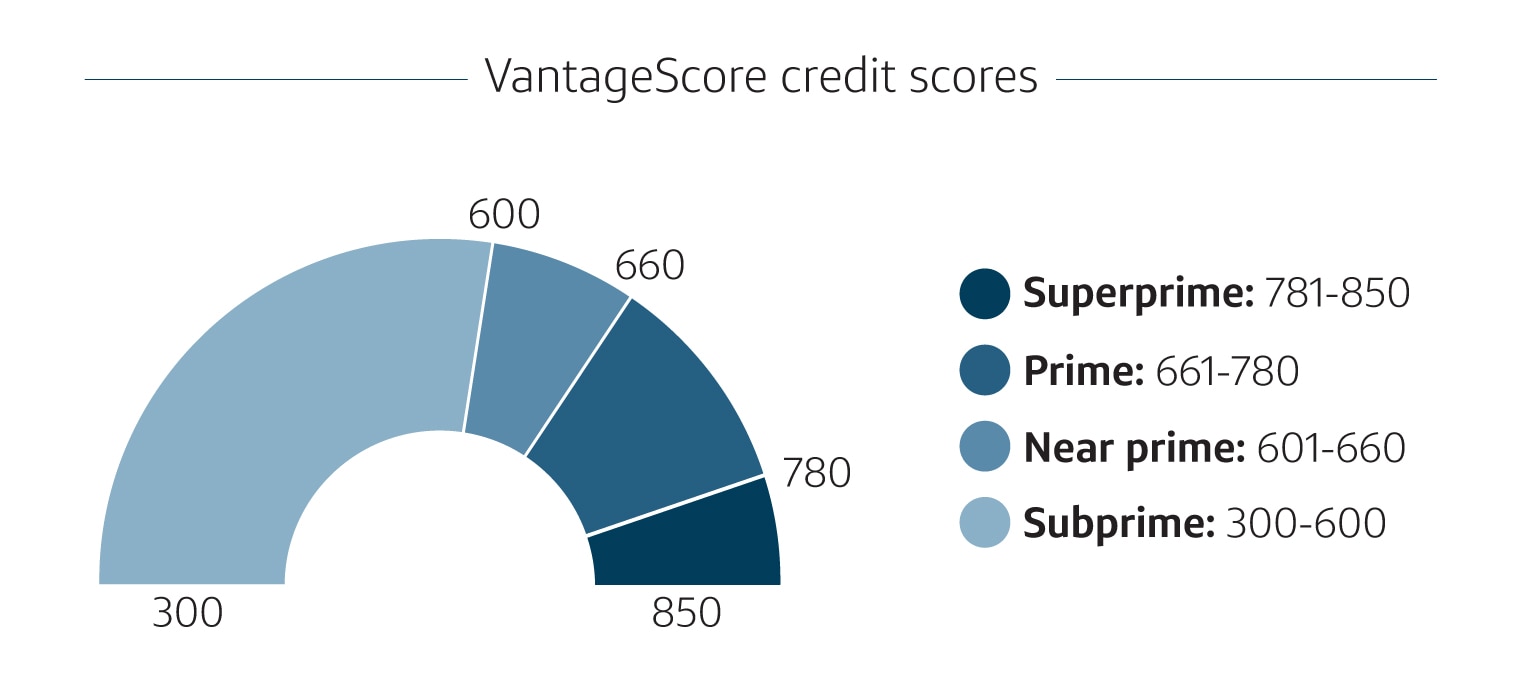

What is a good VantageScore?

A good VantageScore falls between 661 and 780. For VantageScore 3.0 and 4.0, the highest credit score is 850. VantageScore breaks its scores into four groups and uses credit ranges and category names different from those of FICO:

Source: VantageScore.com

-

Superprime: 781-850

-

Prime: 661-780

-

Near prime: 601-660

-

Subprime: 300-600

What affects your credit scores?

Credit-scoring models and credit reports are two big factors that determine your credit score. But if you don’t know what information from your credit report is being used, it’s not much help.

Here are a few factors found in credit reports that typically impact credit scores:

-

Payment history

-

Debt

-

Credit utilization rate

-

Loans

-

Credit age

-

New credit applications

FICO and VantageScore weigh factors differently. Here’s how FICO ranks them:

-

Payment history: 35%

-

Total debt: roughly 30%

-

Length of credit history: roughly 15%

-

Credit mix: roughly 10%

-

New credit accounts: 10%

Here’s how different scoring factors are ranked in VantageScore 3.0 credit scores:

-

Payment history: 40%

-

Depth of credit: 21%

-

Credit utilization: 20%

-

Balances: 11%

-

Recent credit: 5%

-

Available credit: 3%

And here’s how they’re weighted in VantageScore’s latest credit-scoring model, VantageScore 4.0:

-

Payment history: 41%

-

Depth of credit: 20%

-

Credit utilization: 20%

-

Recent credit: 11%

-

Balances: 6%

-

Available credit: 2%

What factors don’t impact credit scores?

Most credit-scoring models don’t consider certain information unless it’s part of your credit report. And even then, some parts of your credit report won’t impact your scores.

Credit-scoring models generally don’t consider:

-

Your age, race, nationality, color, sex, gender or marital status

-

Where you live and work

-

Your income, your job or whether you’re employed

-

Whether you receive public assistance

-

Political or religious affiliations

-

The interest rates on your credit accounts

Closed and paid-off accounts will stay on your credit reports and can continue to impact your scores until they fall off.

Why is a good credit score important?

Good credit scores are important because your credit scores can affect your ability to qualify for credit, as well as the rates and terms of the credit you do qualify for:

-

A poor to fair credit score could make it more difficult to qualify for many credit cards and loans. If you do qualify for an account, you may have to pay high fees and interest rates if you don’t pay your balance in full each month. You might need to start with a secured credit card or credit-builder loan to build your credit.

-

A fair to good credit score may qualify you for more options, but you won’t necessarily receive the best rates or terms. You might find you can qualify for an unsecured credit card but have a harder time qualifying for a premium card.

-

A good credit score could give you a better chance of qualifying for a card offering benefits like cash back and travel rewards. It may not have the best rates or terms though.

-

A very good, excellent or exceptional credit score could qualify you for the best products with the lowest advertised rates. While creditors consider other factors when determining your eligibility and rates, your credit score likely won’t be what’s holding you back.

4 ways to build good credit

Building and maintaining good credit scores comes down to using credit responsibly over time. Here are some things the CFPB says you can do:

-

Pay your bills on time. Consider setting up automatic payments or electronic reminders to help you remember to make on-time payments.

-

Stay below your credit limit. Experts recommend keeping your credit use below 30% of your available credit across all your credit card accounts.

-

Apply only for the credit you need. If you apply for multiple credit cards and loans over a short period, credit card issuers and other lenders may think your financial situation has worsened.

- Check your credit reports. Because your credit scores are based on the information in these reports, errors can hurt your credit scores.

Compare Capital One credit cards for good vs. excellent credit

Many credit card issuers offer cards for those with good credit scores. And Capital One is no different. So how does a credit card for good credit differ from one for excellent credit? It depends on the specific card, but rates and rewards might not be quite the same as a similar card for people with excellent credit. Cardholders with a Capital One credit card for good credit, for example, are not eligible for an early spend bonus or low intro APR.

Expand the sections below to get a look at how three of Capital One’s credit cards for good credit compare to similar cards for excellent credit.

Savor for Good Credit vs. Savor

Savor for Good Credit and Savor are two of Capital One’s dining and entertainment credit cards. Here’s how they compare:

|

|

Savor for Good Credit |

Savor |

|

Credit score range |

Good |

Excellent |

|

Rewards |

3% cash back at grocery stores and on dining, entertainment and popular streaming services* 1% cash back on all other purchases 8% cash back at Capital One Entertainment 5% cash back on hotels and rental cars booked through Capital One Travel |

3% cash back at grocery stores and on dining, entertainment and popular streaming services* 1% cash back on all other purchases 8% cash back at Capital One Entertainment 5% cash back on hotels and rental cars booked through Capital One Travel |

|

Early spend bonus available |

No |

Yes |

|

Low intro APR |

No |

Yes |

|

Annual fee |

No |

No |

Quicksilver for Good Credit vs. Quicksilver

Quicksilver for Good Credit and Quicksilver are two of Capital One’s cash rewards credit cards. Here’s how they compare:

|

|

Quicksilver for Good Credit |

Quicksilver |

|

Credit score range |

Good |

Excellent |

|

Rewards |

1.5% cash back on every purchase, every day 5% cash back on hotels and rental cars booked through Capital One Travel |

1.5% cash back on every purchase, every day 5% cash back on hotels and rental cars booked through Capital One Travel |

|

Early spend bonus available |

No |

Yes |

|

Low intro APR |

No |

Yes |

|

Annual fee |

No |

No |

VentureOne for Good Credit vs. VentureOne

VentureOne for Good Credit and VentureOne are two of Capital One’s travel rewards credit cards. Here’s how they compare:

|

|

VentureOne for Good Credit |

VentureOne |

|

Credit score range |

Good |

Excellent |

|

Rewards |

1.25X miles on every purchase 5X miles on hotels and rental cars booked through Capital One Travel |

1.25X miles on every purchase 5X miles on hotels and rental cars booked through Capital One Travel |

|

Early spend bonus available |

No |

Yes |

|

Low intro APR |

No |

Yes |

|

Annual fee |

No |

No |

How to monitor your credit score

Credit monitoring can help you detect fraud and track your credit scores.

One way to do this is by using CreditWise from Capital One, which lets you access your credit report and credit score. Using CreditWise won’t hurt your credit scores. And it’s free and available to everyone, even if you don’t have a Capital One account.

You can also get free copies of your credit reports by visiting AnnualCreditReport.com.

Good credit score FAQ

Here are the answers to some frequently asked questions about good credit scores:

How rare is a 700 credit score?

A credit score of 700 isn’t especially rare—roughly 60% of Americans have a FICO score of 700 or higher.

How many people have an 800 credit score?

About 22% of Americans have a FICO score of 800 or higher.

What is a good credit score by age?

Since credit history is a key factor impacting credit scores, older individuals tend to have higher credit scores. According to 2023 data from Experian, here’s a breakdown of average credit scores by age:

| Average credit score by generation | |

| Silent generation (age 78+) | 760 |

| Baby boomers (ages 59-77) | 745 |

| Generation X (ages 43-58) | 709 |

| Millennials (ages 27-42) | 690 |

| Generation Z (ages 18-26) | 680 |

Key takeaways: What is a good credit score?

What’s considered a good credit score may vary among scoring companies and lenders. However, generally speaking, FICO considers scores between 670 and 739 to be good scores—and VantageScore’s equivalent of good scores, which they call prime scores, would fall between 661 and 780.

Using credit accounts responsibly and paying your bills on time can help you establish and maintain good or even excellent credit scores. Having low credit card balances and avoiding late payments could also help you maintain good credit. There are many credit card options available to those with good credit. Find out which cards you might qualify for with pre-approval. It’s quick, only requires some basic info and won’t hurt your credit scores.